Running a business comes with risks. Protecting against those risks is crucial.

General liability insurance helps shield your business from financial losses. Every business, big or small, faces potential lawsuits and claims. These can arise from accidents, injuries, or damages involving customers or clients. Without proper coverage, such incidents can drain your finances.

General liability insurance acts as a safety net. It covers legal costs, medical expenses, and damages. This insurance ensures that a single mishap doesn’t cripple your business. It’s an essential part of a strong risk management strategy. Understanding its benefits and how it works can save your business from unexpected financial strain. Stay prepared and protect your business with general liability insurance.

:max_bytes(150000):strip_icc()/Commercial-General-Liability-Final-51e0c0f9b27d4e409a7f49da59fbe037.jpg)

Credit: www.investopedia.com

Introduction To General Liability Insurance

General liability insurance helps protect businesses from claims. These claims can include bodily injury, property damage, and personal injury. Without it, a business might face high costs. These costs could damage the business. Insurance provides a safety net. It helps in covering legal fees and compensation. This protection can save a business from financial ruin.

Many think general liability insurance covers all risks. It does not cover employee injuries. It does not cover professional mistakes.People also think it’s expensive. But it’s not. Costs depend on the size and type of business. Skipping this insurance can be more costly. Some believe small businesses do not need it. Small businesses are at risk too. They can face the same claims as large ones.

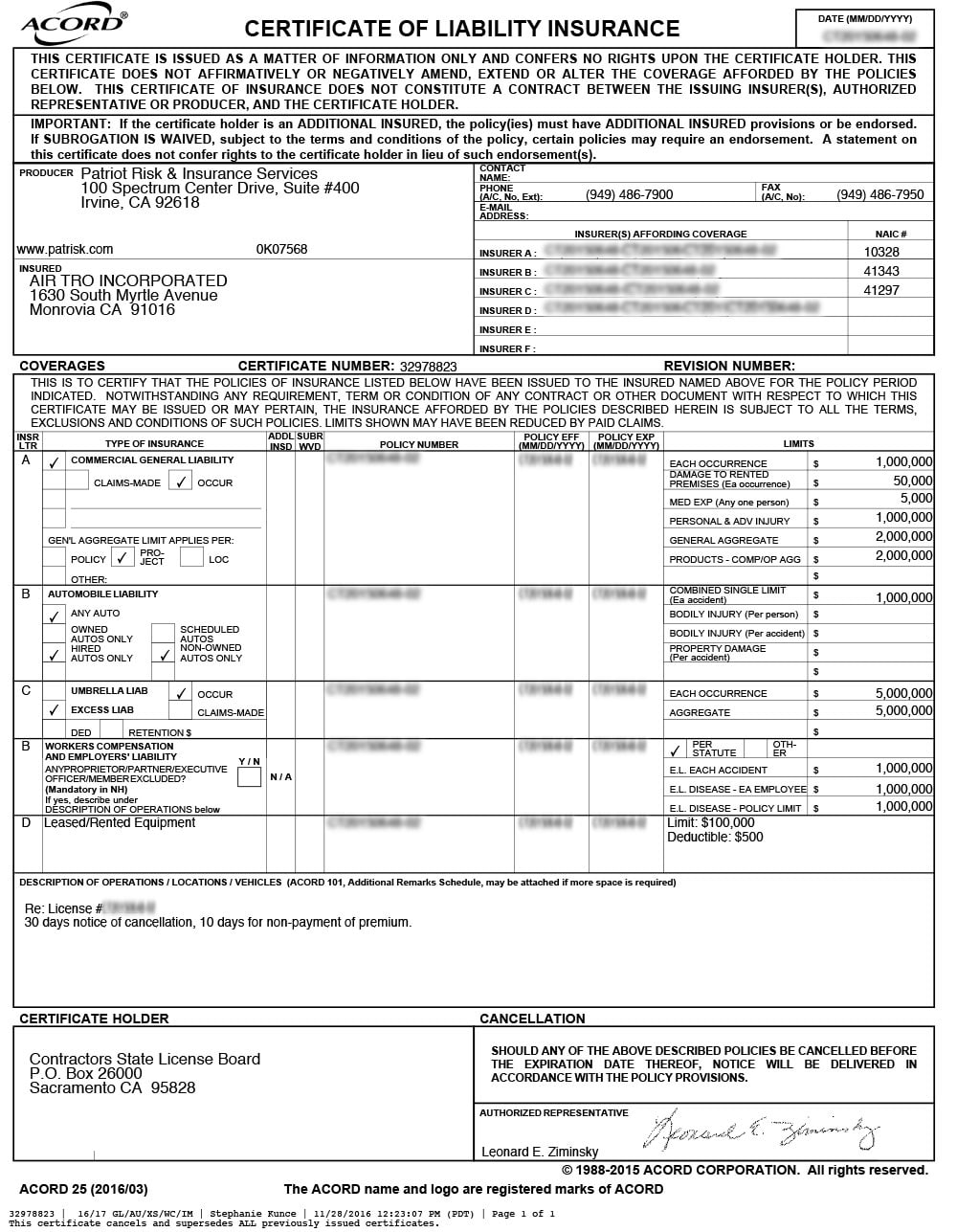

Credit: www.airtro.com

Key Coverage Areas

Bodily injury coverage helps when someone gets hurt at your business. It pays for medical costs and legal fees. This keeps your business safe from big expenses. Always keep this coverage active.

Property damage coverage helps when your business harms someone’s property. It pays to repair or replace the damaged items. This includes things like broken windows or damaged cars. Essential for every business.

Personal and advertising injury coverage is for claims like slander or copyright issues. It protects your business if someone says you hurt their reputation. It also covers legal costs. Important to keep your business safe.

Determining Your Coverage Needs

Assessing business risks is vital. Identify all possible threats. These could be accidents, theft, or lawsuits. Evaluate each risk carefully. Some risks may be higher than others. Create a risk management plan. This helps in reducing potential problems.

Each industry has unique needs. Research your industry’s standards. Some sectors need more coverage. Ensure your policy meets all requirements. This keeps you compliant and safe. Consult with industry experts if unsure.

Credit: www.thehartford.com

Choosing The Right Policy

Finding the best general liability insurance can be tricky. Start by looking at different providers. Compare their coverage options. Check how much each policy costs. Don’t just look at the price. Quality matters too. Read reviews from other businesses. They can tell you a lot. Also, ask for quotes from different companies. This helps you see who offers the best deal. Make sure to ask questions. Understand what each policy covers and what it does not. This way, you can make the best choice for your business.

Always read the fine print. It contains important details. Look for exclusions. These are things the policy does not cover. Also, check the limits. This is the maximum amount the insurance will pay. Know the deductibles too. This is what you pay before the insurance starts to pay. Understanding these terms is key. It helps you avoid surprises later. Ask your provider to explain if anything is unclear. This way, you know exactly what you are getting.

Cost Factors

The size of your business impacts the premium. Larger businesses often pay more. Industry type also affects cost. High-risk industries face higher premiums. Your claims history matters too. More claims can lead to higher costs. Employee numbers are another factor. More employees mean higher premiums. Location plays a role as well. Some areas have higher rates. Finally, coverage limits affect premiums. More coverage means higher costs.

Keep a clean claims history to lower costs. Train employees to avoid accidents. Safety programs help reduce risks. Choose higher deductibles to save money. Bundle policies for discounts. Work with an agent to find the best rates. Regularly review your coverage needs.

Claims Process

First, contact your insurance provider. Tell them about the incident. They will ask for details. Provide all needed information. This may include photos and witness statements. They will give you a claim number. Keep this number safe. It will help track your claim.

An adjuster will be assigned. They will review your case. They may ask more questions. Be ready to provide additional documents. The adjuster will determine if the claim is valid. If valid, they will decide the amount you will receive.

Once approved, you will get the payment. This may cover repairs or medical bills. It is important to follow up with your provider. Make sure everything is processed correctly. This will help you get your money faster.

Common Exclusions

General liability insurance does not cover intentional acts. If someone causes harm on purpose, the insurance won’t pay. This is to prevent misuse. Businesses must act responsibly. Avoiding intentional harm is key. Insurers expect ethical behavior. Accidents and mistakes are covered. Deliberate actions are not.

Employee injuries are not covered under general liability. Workers’ compensation insurance covers these. This insurance handles medical bills. It also covers lost wages. General liability focuses on third-party claims. Protect employees with proper coverage. Ensure safety measures are in place. This helps avoid injuries. Proper coverage is essential.

Tips For Maintaining Coverage

Review your policy often. Ensure it fits your business needs. Business changes may require updates. Contact your agent for advice. Keep your policy current. This avoids coverage gaps. Regular checks save you from surprises.

Follow all legal requirements. Keep records updated. Ensure safety standards are met. Regular inspections help. Train your staff well. Compliance avoids legal troubles. Your policy may require specific actions. Understand and follow them.

Real-life Examples

A restaurant faced a slip and fall accident. A customer slipped on a wet floor. The customer sued the restaurant. The restaurant’s general liability insurance covered the costs. This included medical bills and legal fees.

A small business was sued for copyright infringement. The business used an image without permission. The image owner demanded compensation. General liability insurance paid for the settlement. It also covered the court costs.

Always keep floors clean and dry. This can prevent accidents. Use signs to warn of wet floors. This can avoid lawsuits.

Only use images you have rights to. This can prevent copyright issues. Check image licenses before use. This can save money and stress.

Frequently Asked Questions

What Is General Liability Insurance?

General liability insurance protects businesses from claims of bodily injury, property damage, and personal injury. It helps cover legal fees and medical costs.

Why Do Businesses Need Liability Insurance?

Businesses need liability insurance to protect against lawsuits and financial losses. It ensures that unforeseen incidents don’t cripple the business financially.

What Does General Liability Insurance Cover?

General liability insurance covers bodily injury, property damage, and legal expenses. It also includes product liability and advertising injury.

How Much Does General Liability Insurance Cost?

The cost of general liability insurance varies. It depends on business size, industry, and coverage limits. Typically, small businesses pay around $500 to $1,000 annually.

Conclusion

General liability insurance is essential for business protection. It covers legal costs and damages. This insurance helps manage risks and provides peace of mind. Business owners feel secure knowing they are protected. It’s a smart investment for any business. Safeguard your business and focus on growth.

Protect your hard-earned assets today. Don’t wait until it’s too late. Make sure your business has the right coverage.